The plusvalía municipal, in full 'Impuesto sobre el Incremento del Valor de los Terrenos de Naturaleza Urbana (IIVTNU)' is a Spanish municipal capital gains tax on the cadastral appreciation of 'urban land'. By an 'urban' qualification, we mean not only residential properties, but also commercial properties, for example. In practice, 'rustico' properties (agricultural properties) excluded from the tax and thus exempt.

Learn more about the municipal capital gains tax here.

When do I pay plusvalía municipal?

You pay this tax when you transfer property with an 'urban' qualification, either through sale, inheritance, gift or other form of transfer.

The declaration deadline is 1 month after the transfer. For estates, the deadline is 6 months after death, with the possibility of extension.

Who pays for the plusvalía municipal?

The taxpayer is the transferor in the case of a sale or gift, or the heir in the case of an inheritance. Exceptions apply, for example, to the transfer of property between spouses as part of a divorce. When the seller is a non-resident, the buyer will deduct the tax payable from the purchase price.

How is the plusvalía municial calculated?

The municipal capital gains tax is calculated based on the cadastral value of the land and the number of years the transferor has owned the land. The cadastral value of the land is an estimate of the value of the land by the government and is independent of the sales value of the structure or building that may be on the land.

The rate varies by municipality and is applied to the taxable base. Municipalities have a degree of autonomy to set these tax rates within the limits set by law. The maximum rate is 30%.

The Spanish Constitutional Court has issued several rulings in recent years in which it declared the application of the tax unconstitutional in situations where there was no actual increase in the value of the land or where the fee to be paid exceeded the actual increase in value. This led to changes in the regulations to adjust the tax to the economic reality of each transaction, resulting in two calculation methods. The first method is still based on the cadastral capital gain. The second method is through actual capital gains.

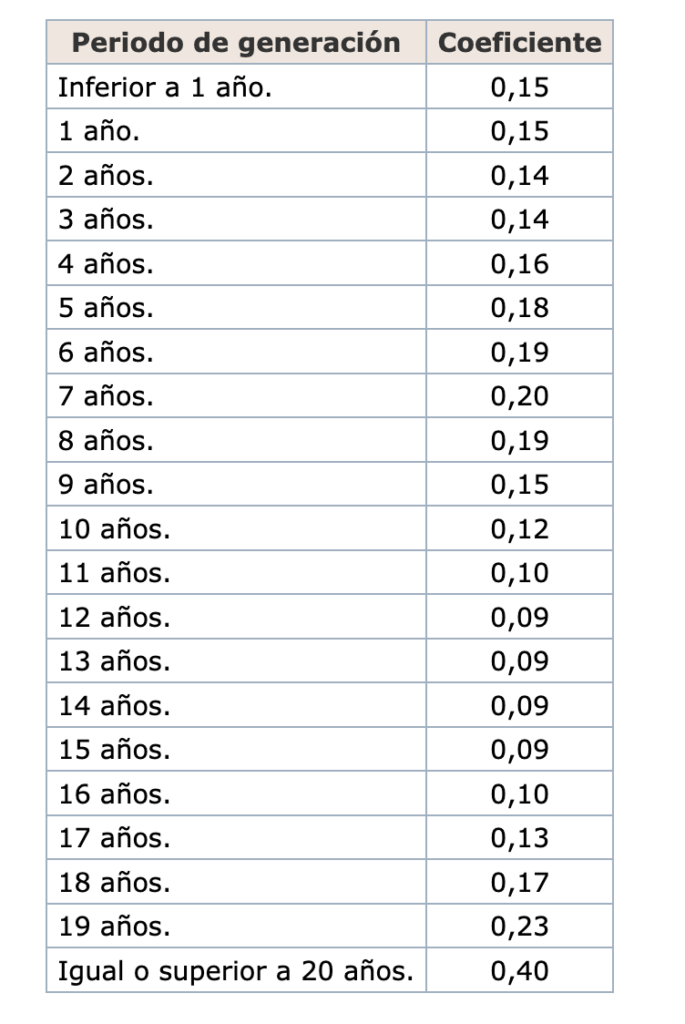

Calculation method of cadastral surplus value

The cadastral capital gain is calculated using a coefficient. This coefficient depends on the number of years the property has been owned by the transferor and can you consult the table of coefficients published annually (Article 24, or see the table below). You multiply the cadastral value of the land by the appropriate coefficient. Then you apply the municipal rate, with a maximum of 30% to arrive at the tax.

An example. You sell a flat with a cadastral value of 120,000 euros. The sale price is 220,000 euros and you realise a capital gain of 60,000 euros. The cadastral land value comes to 30,000 euros. You have already owned the flat for 5 years, so the coefficient is 0.18. Your municipality's rate is 20%. The plusvalía municipal then comes to €30,000 * 0.18 * 20% = 1,080 euros.

Calculation method of actual capital gains

In case you choose this method, you need to calculate the actual capital gain on the land value. You do this based on the ratio of the cadastral land value to the total cadastral value. You then multiply this percentage by the realised value. From this, you apply the municipal rate to arrive at the tax payable.

Let's take the above example again. You sell a flat with a cadastral value of 120,000 euros. The sale price is 220,000 euros and you realise a capital gain of 60,000 euros. The cadastral land value comes to 30,000 euros. The land value ratio is 30,000/120,000 = 25%. You then take 25% from the realised capital gain of €60,000 = €15,000. The rate is 20%, so the tax payable is 3,000 euros amounts.

This calculation method is therefore generally less interesting than the calculation based on cadastral capital gains, unless, of course, you do not realise added value. The tax on a sale at a loss will be €0.

Not the same as national capital gains tax

The plusvalía municipal should not be confused with the national capital gains tax ('impuesto sobre la ganancia patrimonial'). This capital gains tax is calculated on the capital gains actually realised and applies to all transfers of property, among other things, excluding inheritances.

Learn more about Spain's national capital gains tax here.

Decision

In summary, the plusvalía municipal is a tax payable on the sale, inheritance or gift of urban land in Spain. Its calculation is based on (i) either the increase in value of the land over time, according to the cadastral value and annually fixed coefficients or (ii) on the actual capital gain. If you are transferring at a loss, it is better to opt for the second method.

If you have any questions about selling or gifting property in Spain. If so, please feel free to contact with us.